Desert Online General Trading LLC

Warehouse # 7, 4th Street, Umm Ramool, Dubai, 30183, Dubai

Desert Online General Trading LLC

Warehouse # 7, 4th Street, Umm Ramool, Dubai, 30183, Dubai

Full description not available

I**R

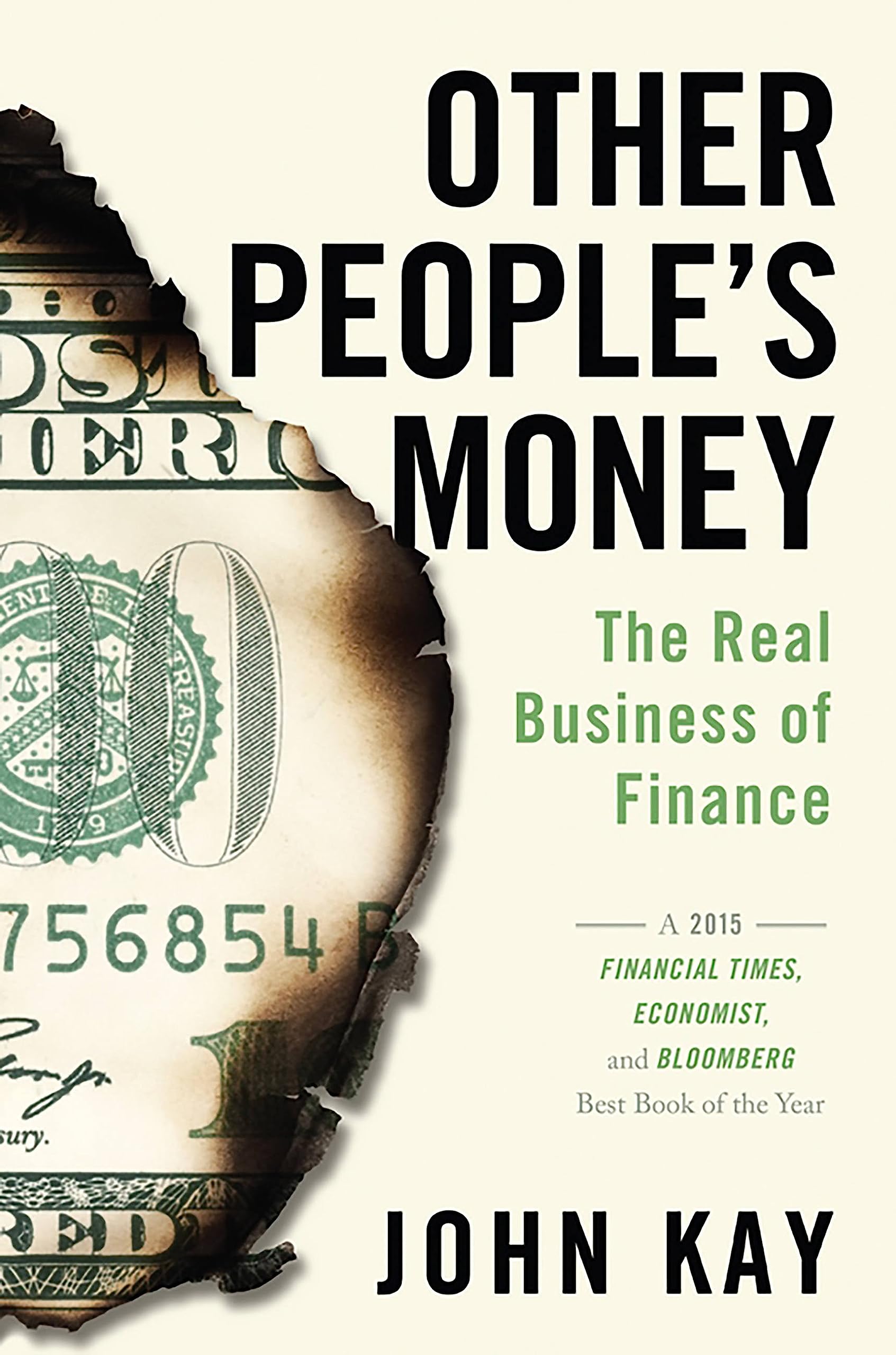

By far the best book I have read on what's wrong with our financial institutions.

A real rarity--a book about finance that is both iinstructive and fun to read. Kay is an extremely good writer, who uses simple analogies to underscore his points. The tailgating ultra-high-speed French driver becomes the example of risking a calamity to gain a small advantage. A graphic image which is far better than pages of discussion of risk analysis.I have read several books about the 2008 collapse. This is by far the best of the bunch, providing a clear road map to the problems of the financial industry which made its collapse inevitable. And which will provide another crisis unless the political class can force real change.The basic problem is that too many of the financial institutions have stopped providing a useful service to the society, and become gamblers using the public's money to gamble. That I had realized. And I knew that if the gambles went sour, the Central Banks were ready to pour new money into the institution., so the hapless public covered the downside.;, But I had thought that the profits from the gambling would go to the shareholders. Not so. What I hadn't understood is that most of the profits are paid over to the executives as citizen-infuriating salaries, and to the gamblers who had won their bets, as bonuses.Kay doesn't offer what is, to me, a plausible solution. The key, as he says, is to separate the gamblers from public money and government bail-outs. Sounds a lot like Glass-Stegall, which got the job done for 75 years, but was finally nullified just in time to permit the gamblers to bring us the 2008 disaster; and couldn't get past the bank lobbyists as Congress pretended to look for solutions. So they get Elizabeth Warren's Consumer Protection Board. The Lord works in mysterious ways.

A**R

Worth Reading, but a Little Muddled and Here and There Suspect

I was looking for a book to provide a critical but reasonably unbiased overview of the finance industry, chose this one, and am not disappointed. John Kay is a good guide. He not only knows the minutia, but also keeps the focus on the basic tasks that we want and need finance to perform. It's a well-balanced, informative book that fortunately isn't difficult for industry outsiders like me to understand.However, I suppose because I had read glowing reviews of this book before I bought it, I was a tad disappointed when I read it myself (and thus don't give it the full five-star rating). The problem, to my mind, is organizational. This is usually the hardest part of writing any book, and you can tell that Kay (as well as perhaps his editors) worked hard to create a strong organizational structure, but it's still a bit disorganized. Kay frequently refers back to previous points or anticipates future points, writing, for example, "as was discussed in chapter 3" or "as will be discussed in chapter 9." As a writer myself, I know that remarks like these scream, "Weak organization!" A really good writer doesn't do this, but rather figures out a way to cover a point thoroughly when it is brought up, instead of constantly referring the reader somewhere else.The consequence of these organizational weaknesses is to muddy up the priorities of the various points. Reading this book reminded me of taking a course (from a good professor) that meets maybe three times a week for an hour over a semester. In each class, the professor makes good points, but some days the points made are more important than the points made on other days, yet the equal time given to the various points on different days makes it difficult to know which points are more important than others. "Other People's Money" struck be as suffering from this difficulty of weighting the priorities of the various points.Maybe it's just my taste, but I felt that the book would have been better with fewer but longer chapters that were each anchored in a broad theme, under which subsidiary points were prioritized. As it is, the book reads a bit like the linear presentations of lectures.But this criticism isn't a huge gripe, and the book isn't disorganized. I just think that for the book to have been excellent, the organization needed to be improved.And while I'm griping, I have a couple other small quibbles. One is that while Kay seems to have a wise grasp of human nature (something people in economics now deny that they talk about, even though they do), he periodically rests arguments on his sense of human nature that is probably debatable. Those in other social sciences would be reluctant to advance these arguments as easily as Kay does, and if they did, they would pause to develop them. I don't disagree with Kay, but he is a bit fast and loose with assumptions that others might question.My second small (and not unreated) quibble is Kay's failure to deal with discriminatory practices in lending. He makes a strong case (with which I agree) for the importance of lenders knowing their borrowers and making loans based in part upon the borrower's characters, but he completely ignores the reality that this practice has had and frequently still has discriminatory results. Good Old Boy white bankers have a tendency to evaluate the characters of other Good Old Boy whites more highly than they do of ethnic minorities and women, making it incumbent upon anyone who argues that lenders should focus on character to deal with the problem that lenders routinely misjudge character. Indeed, while it's funny and I get his point, Kay even celebrates the days when financial deals were hammered out on the "19th hole" of the golf course. Well, that's great for the customers who play golf, but what about the customers who don't but shoot hoops in the 'hood instead? Must they learn to play golf before they qualify for loans, or should bankers be forced to learn to play baskeball as a nondiscriminatory condition of becoming bankers?It's usually unfair to criticize a book for what it doesn't cover, and it gets tiring when people inject the race-class-gender trinity into discussions of issues where they are tangents. However, Kay is the one who emphasizes the importance of lenders judging borrowers' characters and even illustrates that with golf. Since he does, he is obligated to deal with the usual discriminatory consequences of that approach, but he doesn't even mention them.Overall, though, this book is a good overview of the finance industry and Kay is a good guide.

L**.

There is a lot to learn from this book

Really found this book insightful and thought-provoking. I'm probably a little too young and not well versed enough in finance to have understood everything, which is to say, at times it was a little over my head. However, for it being a finance book, it was rather engaging and I liked the writing style of the author. He seemed like an exceptionally smart and reasonable guy and I found the arguments he presented in the book to be very sensible. It helped that this book didn't have an overt political sway, in fact, I found it difficult to figure out exactly where the author stood. So don't be afraid that if you read this book you're going to be necessarily politically persuaded in some way or another, as it's not really focused on that. The author was also able to describe our financial system almost in a detached, very critical and observational type of way but, as well, he also had an insiders perspective. The gist is that our financial system is too complex and interdependent and this is the source of it's underlying fragility. As well, we have a lot of misconceived regulation. Overall, I really appreciated what I learned from this book, definitely buy it if you are unsure. It's very relevant.

Trustpilot

2 days ago

2 months ago